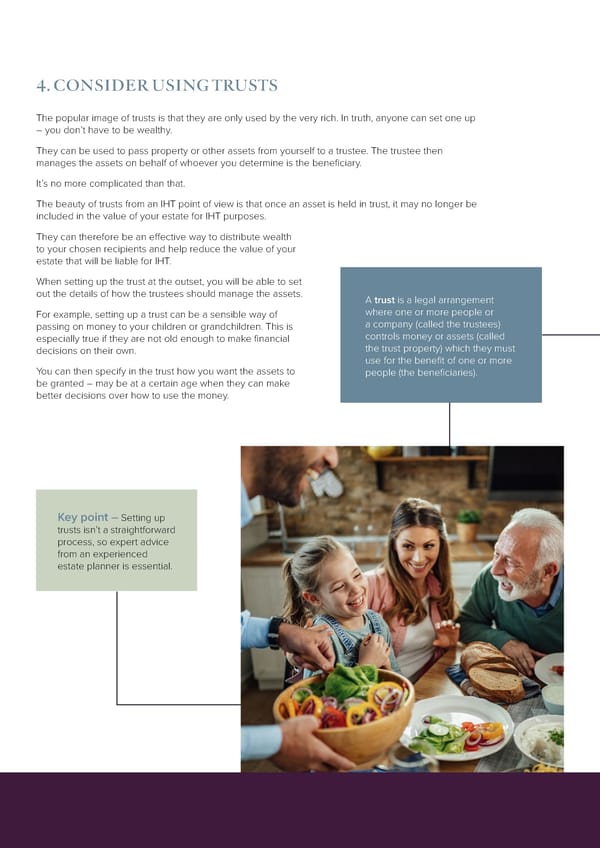

4.CONSIDER USING TRUSTS The popular image of trusts is that they are only used by the very rich. In truth, anyone can set one up –you don’t have to be wealthy. They can be used to pass property or other assets from yourself to a trustee. The trustee then manages the assets on behalf of whoever you determine is the beneficiary. It’s no more complicated than that. The beauty of trusts from an IHT point of view is that once an asset is held in trust, it may no longer be included in the value of your estate for IHT purposes. They can therefore be an effective way to distribute wealth to your chosen recipients and help reduce the value of your estate that will be liable for IHT. When setting up the trust at the outset, you will be able to set out the details of how the trustees should manage the assets. A trust is a legal arrangement For example, setting up a trust can be a sensible way of where one or more people or passing on money to your children or grandchildren. This is a company (called the trustees) especially true if they are not old enough to make financial controls money or assets (called decisions on their own. the trust property) which they must use for the benefit of one or more You can then specify in the trust how you want the assets to people (the beneficiaries). be granted – may be at a certain age when they can make better decisions over how to use the money. Key point – Setting up trusts isn’t a straightforward process, so expert advice from an experienced estate planner is essential.

8 Practical Ways to Ensure Your Family Get More of Your Wealth Than the Taxman Page 8 Page 10

8 Practical Ways to Ensure Your Family Get More of Your Wealth Than the Taxman Page 8 Page 10